This is the second in a series of posts reviewing excerpts of the 2021 Big Broadcast Survey (BBS) and the first post about how the brands of technology suppliers were ranked by respondents to the 2021 BBS.

The previous article about the 2021 BBS reviewed the most important technology trends. For the second article, we are beginning the review of brand rankings of media technology suppliers with the metric of ‘Easy to Work With.’

We started tracking ‘Easy to Work With’ in 2019 in response to developments in the media technology sector. As customer and supplier relationships evolved away from one characterized by building and shipping product to one more characterized by working with customers to solve problems, clients wanted a reference on how relatively ‘Easy to Work With’ they were perceived as being by technology buyers (versus market benchmarks).

At the same time, we were keen to better explore a clear statistical relationship emerging in the data gathered in the Big Broadcast Survey. Across all languages, regions, and product categories a supplier perception highlighted by certain sub-optimal attributes, most notably ‘arrogance,’ had a strong negative relationship to a customer’s willingness to recommend a supplier. In more direct terms, difficult to work with meant unlikely to recommend, regardless of the relative merits of the product offering. (The preceding is a simplified explanation of a necessarily long series of charts).

For these reasons we added the tracking of ‘Easy to Work With’ into the annual Big Broadcast Survey. The events of 2020 (lingering into 2021) made it all the more pressing to understand.

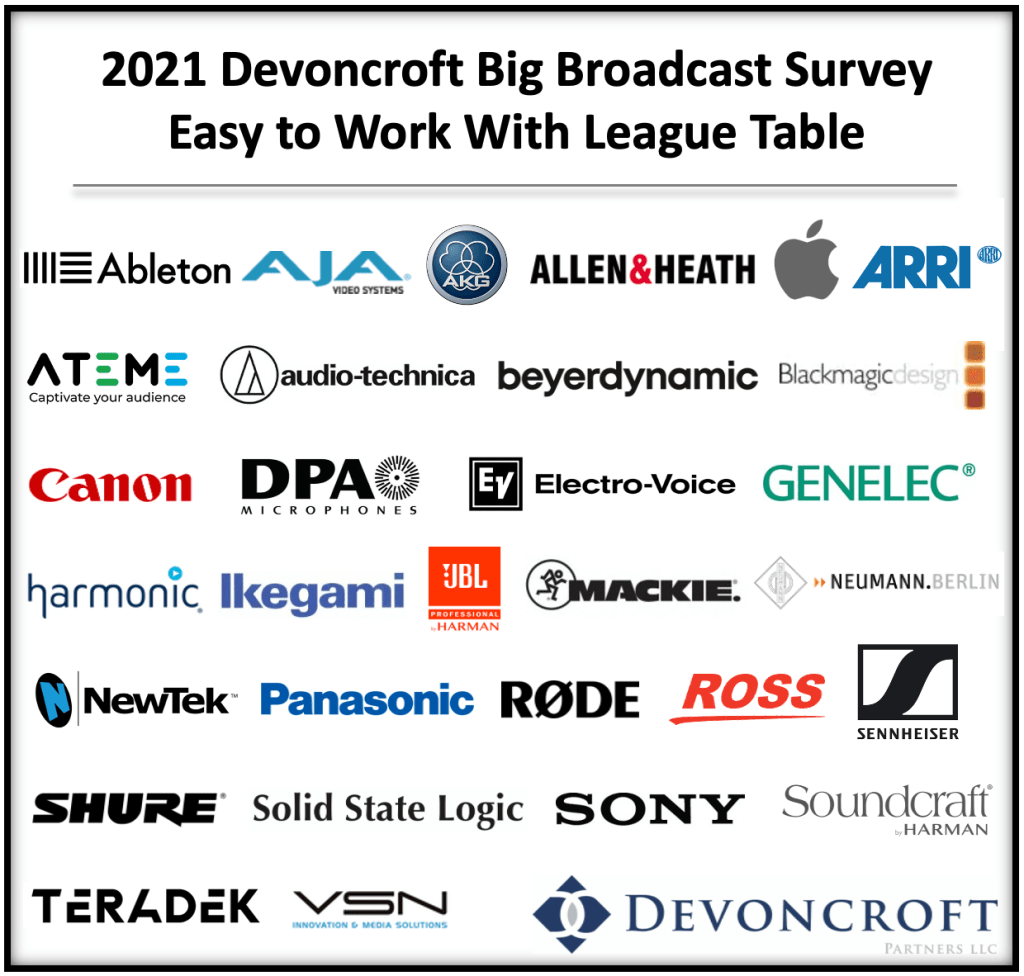

The ‘Easy to Work With’ findings in the 2021 BBS are shown below as an overall industry league table containing the 30 highest ranked suppliers for the metric ‘Easy to Work With.’

An explanation of how these results were calculated can be found at the end of this article. Please note that both audio and video brands are included in these rankings, and that the table below shown brands in alphabetical order, NOT in the order in which they were ranked in the study.

There are a wide variety of companies on this list. Exceptionally large companies such as Apple, Canon, Panasonic, and Sony. Several subsidiaries are represented including NewTek (Vizrt), Soundcraft (Harman/Samsung), and Teradek (Vitec Group). Independent companies like Aja Video, Blackmagic Design, and Genelec are also present.

As alluded above, how these rankings relate to a customer’s purchase decision is an important aspect of interrupting the data. A more detailed review of the relationship is available to clients of the BBS reports.

Provided as a year-over-year reference, below is the 2020 league table for ‘Easy to Work With.’

The 2020 and 2021 league tables for ‘Easy to Work With’ have 12 common members. 18 new members came into the 2021 league table and, equivalently, 18 members of 2021 league table were not present in the 2020 version.

How These Results Were Calculated

2021 BBS participants (and 2020 BBS participants) were asked to provide their perception of how a variety of media technology suppliers ranked in terms of ‘Easy to Work With.’ The scores were measured on a 10-point scale — with 10 being best in the market, and 1 being worst in the market.

This data was then aggregated and averaged in order to generate the global score for each brand based on these responses.

Please keep in mind when reviewing this information that the table is presented in alphabetical order, not in the order brands were ranked by respondents to the BBS. Also, the charts in this posting measure the responses of all 2021 BBS respondents, regardless of their company type, company size, geographic location, job title and budget for media technology products.

In order to get full value from this data, it is necessary to evaluate these results on a granular basis. If you would like more information, please contact Devoncroft Partners.

Please also note that inclusion of any brand in the above table is dependent on inclusion in the 2021 BBS and available sample size. The minimum sample size for inclusion in this charts is 30 respondents. Therefore it is possible that a highly regarded brand was excluded from these findings based on sample size.

The information in this article is based on select findings from the 2021 Big Broadcast Survey (BBS), a global study of media technology industry trends, technology purchasing plans, and benchmarking of media technology vendor brands. Several thousand media professionals in 100+ countries took part in the 2021 BBS, making it the largest and most comprehensive market study ever conducted in the media industry.

Related Content:

2021 Big Broadcast Survey Global Trend Index

© Devoncroft Partners 2009 – 2021. All Rights Reserved.

Discover more from Devoncroft Partners

Subscribe to get the latest posts sent to your email.